|

ACCOUNTING EXERCISES AND PROBLEMS:

Brief Exercises, Exercises, and Problems in textbook for each Summary Note/Chapter can be found in Google Classroom NEW ACCOUNTS: As we learn about new accounts, use this document as a reminder: New Accounts ACCOUNTING FORM TEMPLATES: Full T-Account Ledger and Forms Long Form Balance Sheet General Ledger Chart of Accounts, General Journal, & Financial Statements |

Target Numbers & Solutions

Practice Question Target Numbers Practice Question Solutions Summative Assignment Target Numbers Notes: ASSETS LIABILITIES |

Fundamental Accounting Equation

|

Assets: What a business OWNS including cash, accounts receivable (money not yet collected from customers), supplies, land, buildings, equipment, vehicles, etc.

Liabilities: What a business OWES including accounts payable (money not yet paid to suppliers), bank loans, mortgages, etc. Owners' Equity: What a business is WORTH. If all assets were sold and turned into cash, and all liabilities were paid off, what is left over is the value or worth of the business. |

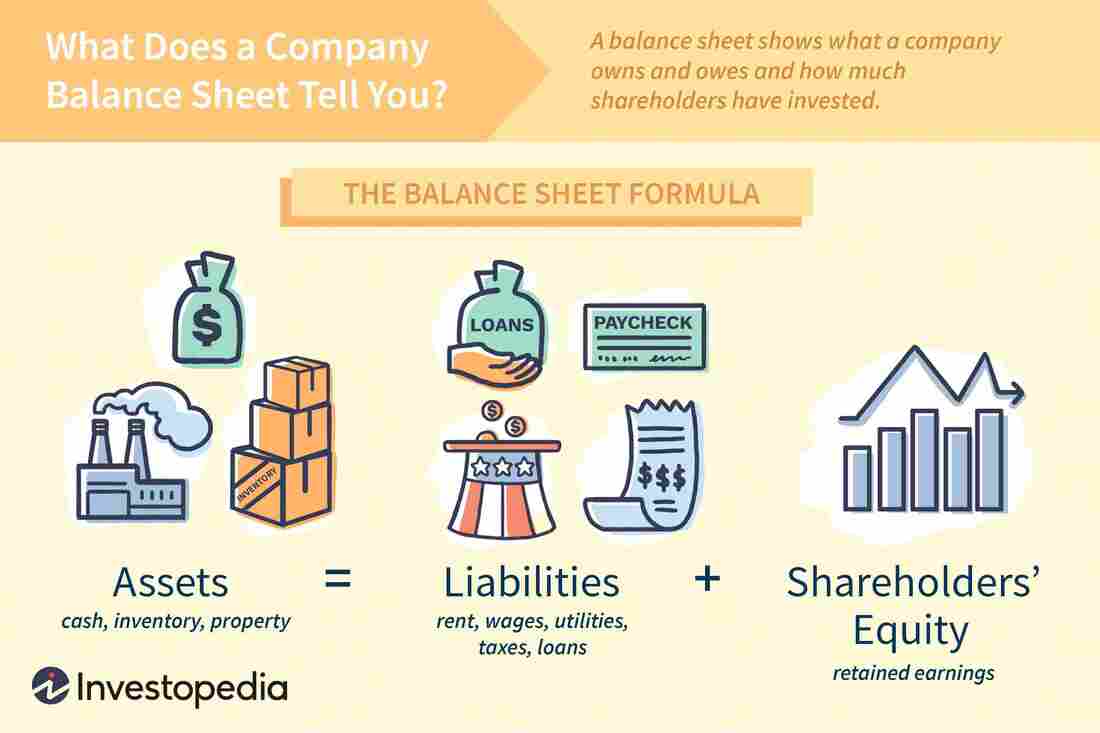

The Balance Sheet

The Balance Sheet is the final, formal accounting document prepared by a business to show all its permanent accounts including assets, liabilities, and owners' equity. It is a snapshot of a business's financial position only for the date it is prepared.

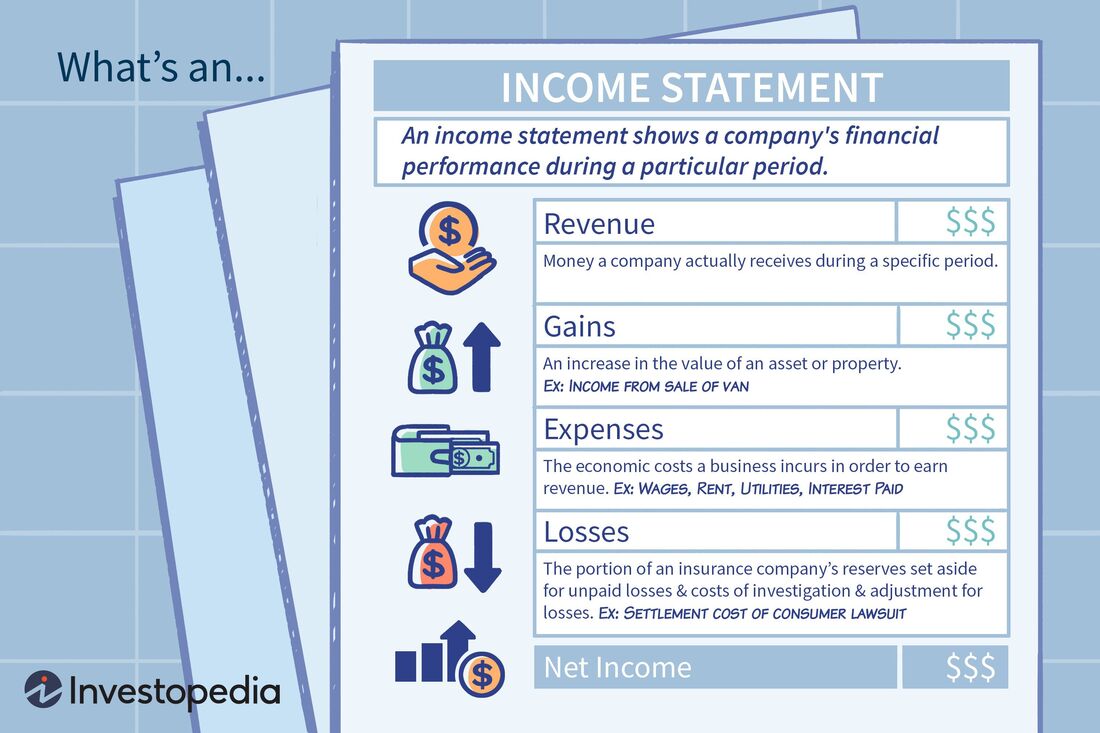

The Income Statement

The Income Statement is a formal accounting document prepared by a business to show its profitability. It is a profit and loss statement that increases (profit) or decreases (loss) the owner's equity or worth of the business. The income statement primarily focuses on the company's revenues and expenses during a period of time.

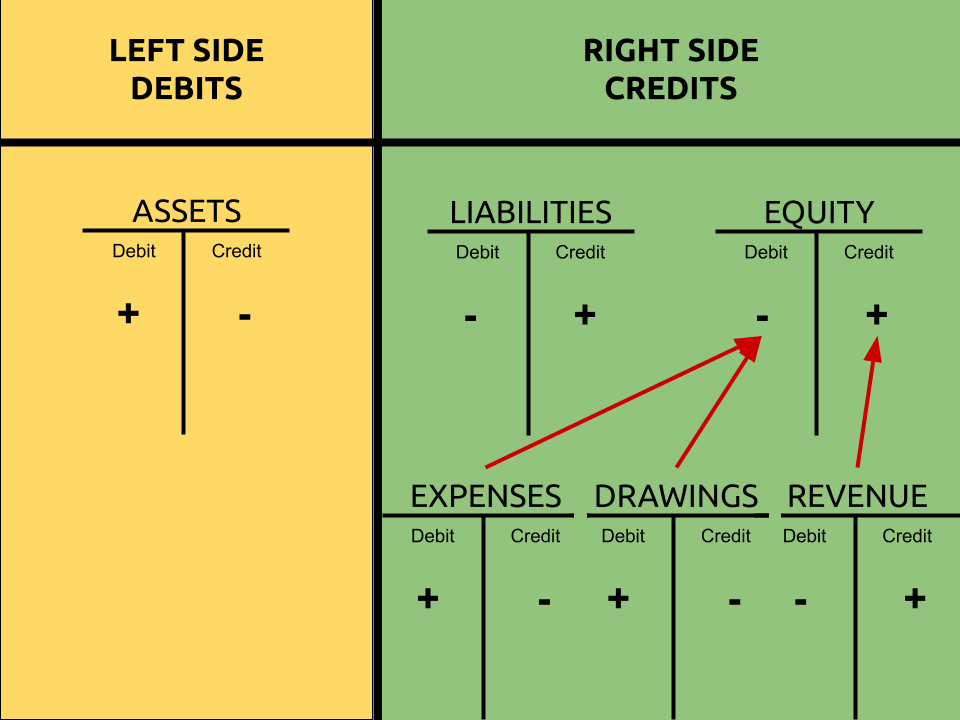

Debits & Credits

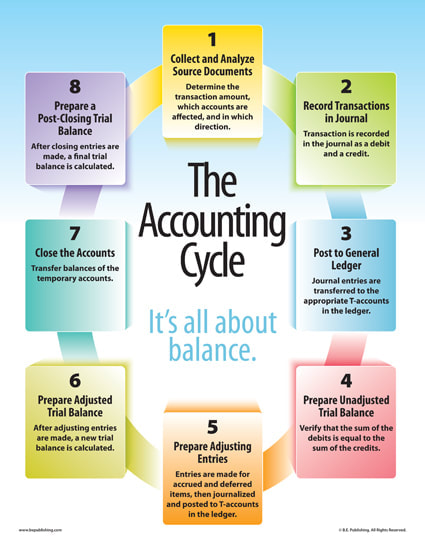

The Accounting Cycle

As soon as a single TRANSACTION occurs, the financial position of a company changes. All transactions are recorded (journalized and posted) and after a period of time (1 year or less), profitability is measured and the ACCOUNTS of the business are balanced to begin a new period.. This process is referred to as the ACCOUNTING CYCLE.